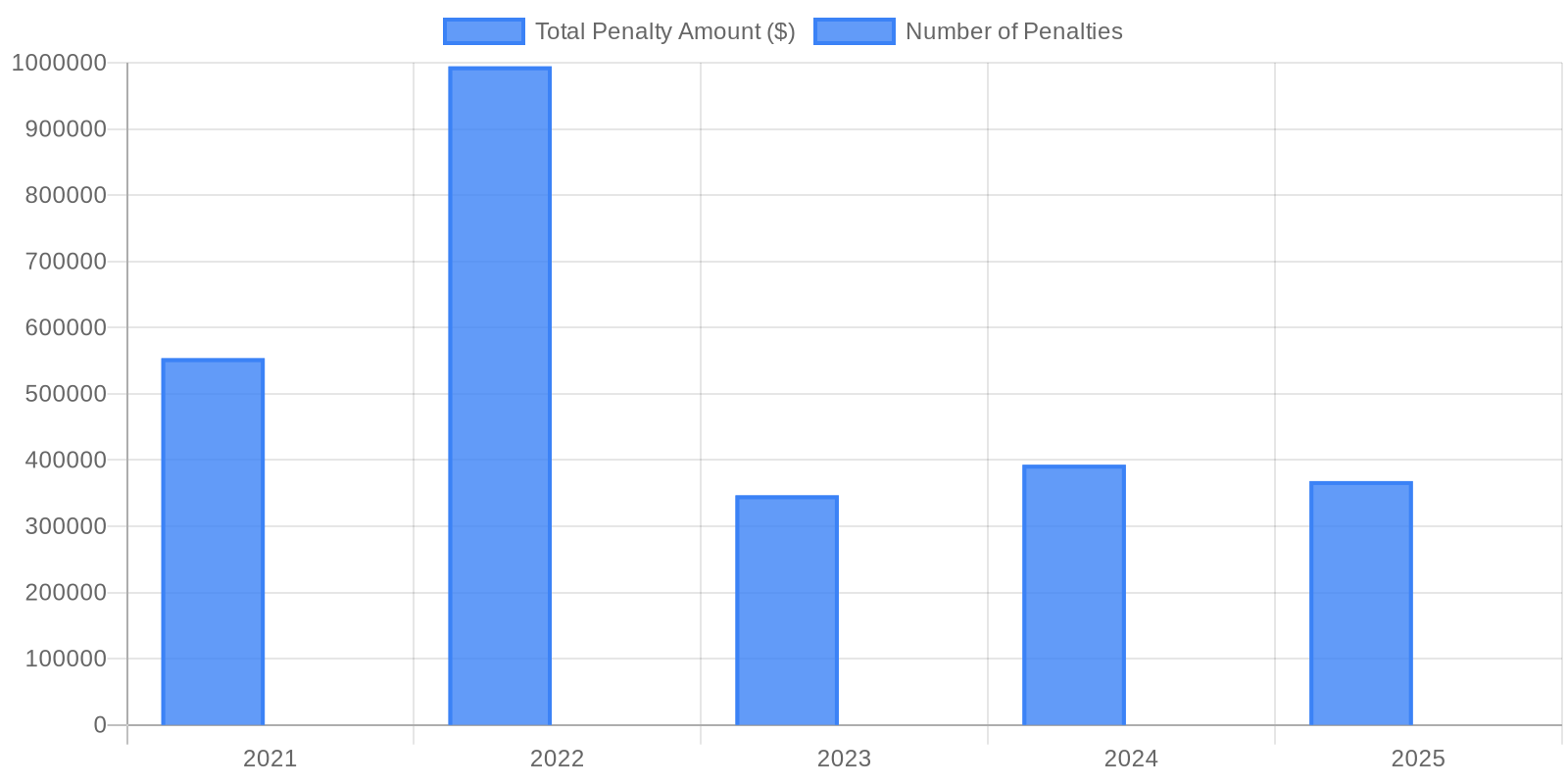

Administrative Monetary Penalties (AMPs) imposed on Canadian real estate brokers from 2021-2025 show fluctuating enforcement, with 2022 recording the highest penalty amount at nearly $1 million despite fewer violations.

Canada's real estate brokerages are facing intensified regulatory scrutiny as FINTRAC has imposed 24 penalties totaling more than $2.6 million since 2021, with most violations tied to weak documentation, governance, and training. The Globe and Mail reports that heavy fines against real estate brokerages for violating federal anti-money laundering rules have many in the industry questioning whether their existing compliance programs are adequate. According to an MNP analysis, the most common issues involved policies and procedures, with FINTRAC finding many firms did not sufficiently address obligations such as ongoing monitoring of business relationships, third-party determinations and recordkeeping requirements. The Government of Canada's 2025 Assessment classified the real estate sector as high risk for money laundering and terrorist financing.

The MNP report reveals concerning patterns across penalized brokerages. Missing or incomplete client information, including full addresses and occupations, was among the most frequently cited issues, while FINTRAC also noted missing receipt-of-funds details such as account numbers, account types and account holder names. Governance gaps were another recurring theme, with nine brokerages having either not appointed a compliance officer or naming one without ensuring the individual had sufficient authority or resources to perform the role. Seven of the 24 brokerages failed to submit suspicious transaction reports despite indicators of suspicious activity, while one brokerage did not file a required large cash transaction report. The largest single penalty reached approximately $282,000, while the average fine was roughly $110,000.

While the penalties demonstrate enhanced enforcement, the Fraser Institute has extensively documented how regulatory compliance costs can burden Canadian businesses disproportionately. Fraser Institute research found that Canadians spend an estimated $103 billion annually to comply with federal, provincial, and municipal regulations, noting that "government regulation hits our pocketbooks as surely as taxes do but there is shockingly little information available about its cost." The institute notes that administrative costs are only the tip of the regulatory iceberg, with the bulk of regulatory costs incurred by individuals and businesses in the private sector to implement, monitor, and demonstrate compliance. For real estate brokerages, particularly smaller operations, the challenge lies in balancing compliance obligations with operational viability in an already complex regulatory environment.

Looking ahead, proposed Bill C-12 threatens to increase penalties by up to 40 times current maximums, signaling that enforcement will only intensify. MNP emphasizes that "compliance isn't a static obligation but a continuous process of improvement," noting that real estate brokers who make AML oversight part of everyday operations will not only meet regulatory standards but also ensure they are taking proactive steps to prevent their services from being inadvertently misused for money laundering. The report recommends that prescribed reviews should be used as tools to evaluate whether AML programs are effective, warning that without these independent assessments, real estate brokers may overlook program weaknesses until FINTRAC identifies them during an examination, and that conducting timely reviews is one of the most effective ways to test program integrity and prevent costly penalties.