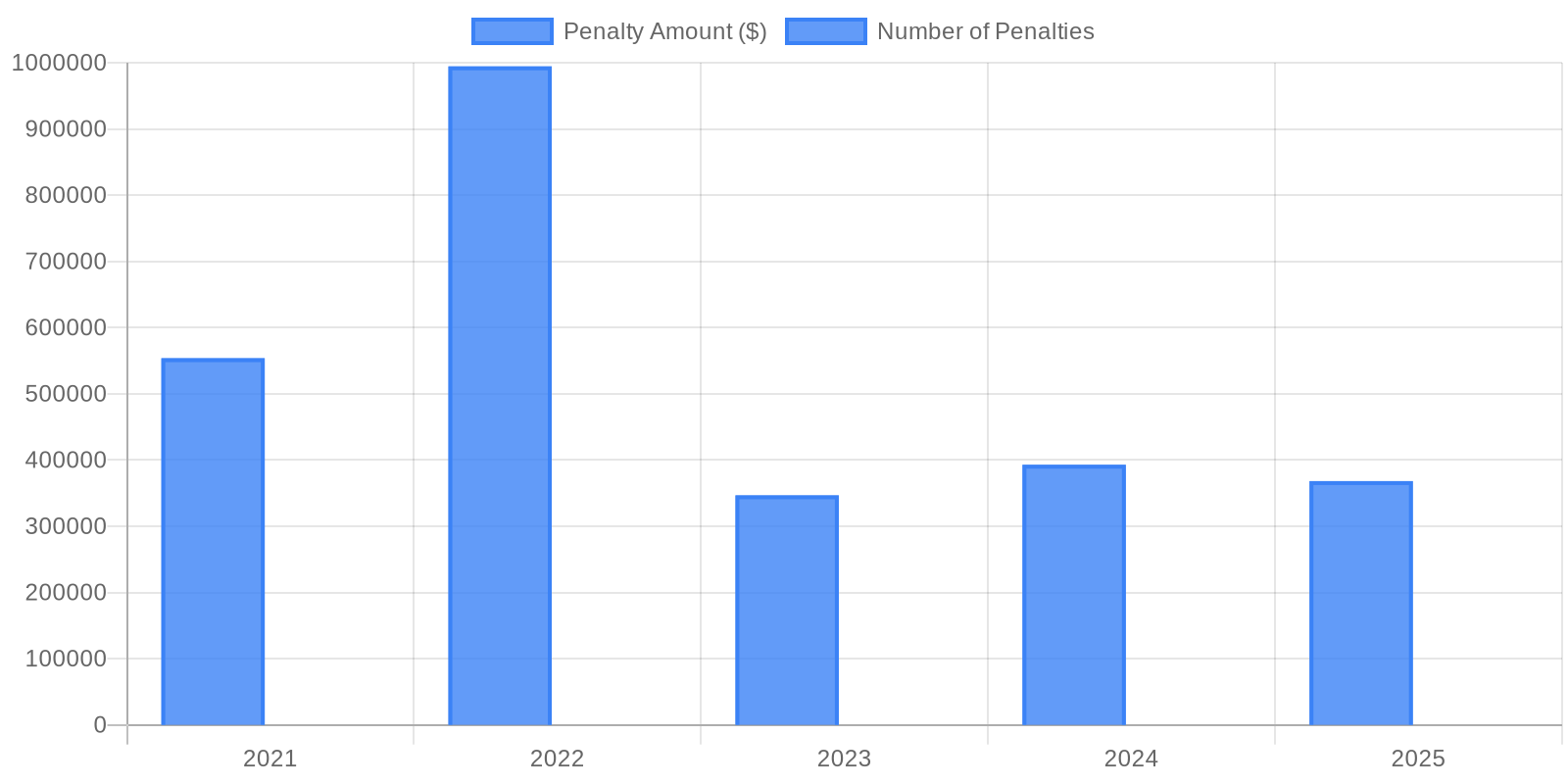

Administrative monetary penalties issued to Canadian real estate brokers peaked at nearly $1 million in 2022 despite fewer violations, demonstrating FINTRAC's shift toward targeting severe compliance failures with substantial financial consequences rather than maximizing penalty volume.

Real estate brokerages across Canada are confronting an unprecedented wave of regulatory enforcement, with FINTRAC expanding its anti-money-laundering scrutiny and 24 firms receiving administrative monetary penalties totaling more than $2.6 million since 2021, with most violations tied to weak documentation, governance, and training. Recent enforcement actions have sent shockwaves through the industry, prompting brokerages to question whether their existing compliance frameworks are adequate. As the Government of Canada's 2025 Assessment of Money Laundering and Terrorist Financing Risks in Canada assessed the real estate sector as high risk, property transactions continue to face heightened regulatory pressure. The compliance pressures are expected to intensify further under Bill C-12 with a proposed increase of up to 40 times the current maximum penalties, signaling a fundamental shift in how Canadian authorities approach financial crime prevention in property markets.

The enforcement data reveals a troubling pattern of systemic compliance failures across Canada's real estate industry. According to detailed analysis from MNP, the violations expose deep-rooted weaknesses in how brokerages approach anti-money laundering obligations. Out of the real estate businesses that received administrative monetary penalties from FINTRAC between 2021 and 2023, 86 percent failed to develop written compliance policies and procedures and keep them up to date, and 86 percent failed to adequately assess and document money laundering risks within their business. Additionally, 64 percent failed to develop and maintain a written ongoing AML compliance training program required by FINTRAC. These deficiencies represent more than technical oversights—they signal a structural disconnect between regulatory expectations and industry practices that has persisted even as Canada's housing market has become increasingly attractive to illicit capital flows.

The compliance crisis unfolds against a backdrop of broader regulatory challenges facing Canada's real estate sector. While Fraser Institute research has extensively documented how costly and challenging land-use regulations have made the housing supply less responsive to demand in Canada's urban centers, the anti-money laundering enforcement wave adds another layer of complexity for an industry already navigating difficult market conditions. The penalty data demonstrates why this matters: while the total number of penalties has remained relatively stable at 5 per year in 2024 and 2025, the 2022 spike to nearly $1 million in fines—despite only 4 penalties—reveals FINTRAC's willingness to impose severe financial consequences for serious compliance failures. Prescribed reviews should be used as a tool to evaluate whether AML programs are effective, as without these independent assessments, real estate brokers may overlook program weaknesses until FINTRAC identifies them during an examination, and conducting timely reviews is one of the most effective ways to test program integrity and prevent costly penalties. The pattern suggests regulators are targeting quality over quantity, focusing enforcement resources on egregious violations that pose genuine money laundering risks rather than pursuing maximum penalty counts.

The intensifying enforcement environment demands a fundamental rethinking of compliance culture across Canada's real estate sector. Compliance isn't a static obligation but a continuous process of improvement, and real estate brokers that make AML oversight part of their everyday operations will not only meet regulatory standards but also ensure they are taking proactive steps to prevent their services from being inadvertently misused for money laundering or related illicit activities. As penalties escalate and regulatory expectations evolve, brokerages face a critical choice: invest in robust compliance infrastructure now or risk far more severe consequences later. The convergence of heightened enforcement, proposed penalty increases, and persistent compliance gaps suggests the industry stands at an inflection point. Those firms that treat anti-money laundering obligations as core business imperatives—rather than regulatory burdens—will be best positioned to navigate the new enforcement landscape while protecting themselves from both financial penalties and reputational damage that could prove far more costly than any compliance investment.