Canadian retail gasoline prices dropped steadily through late 2025 before spiking dramatically in March 2026 due to Middle East conflict, reaching the highest level since September 2024.

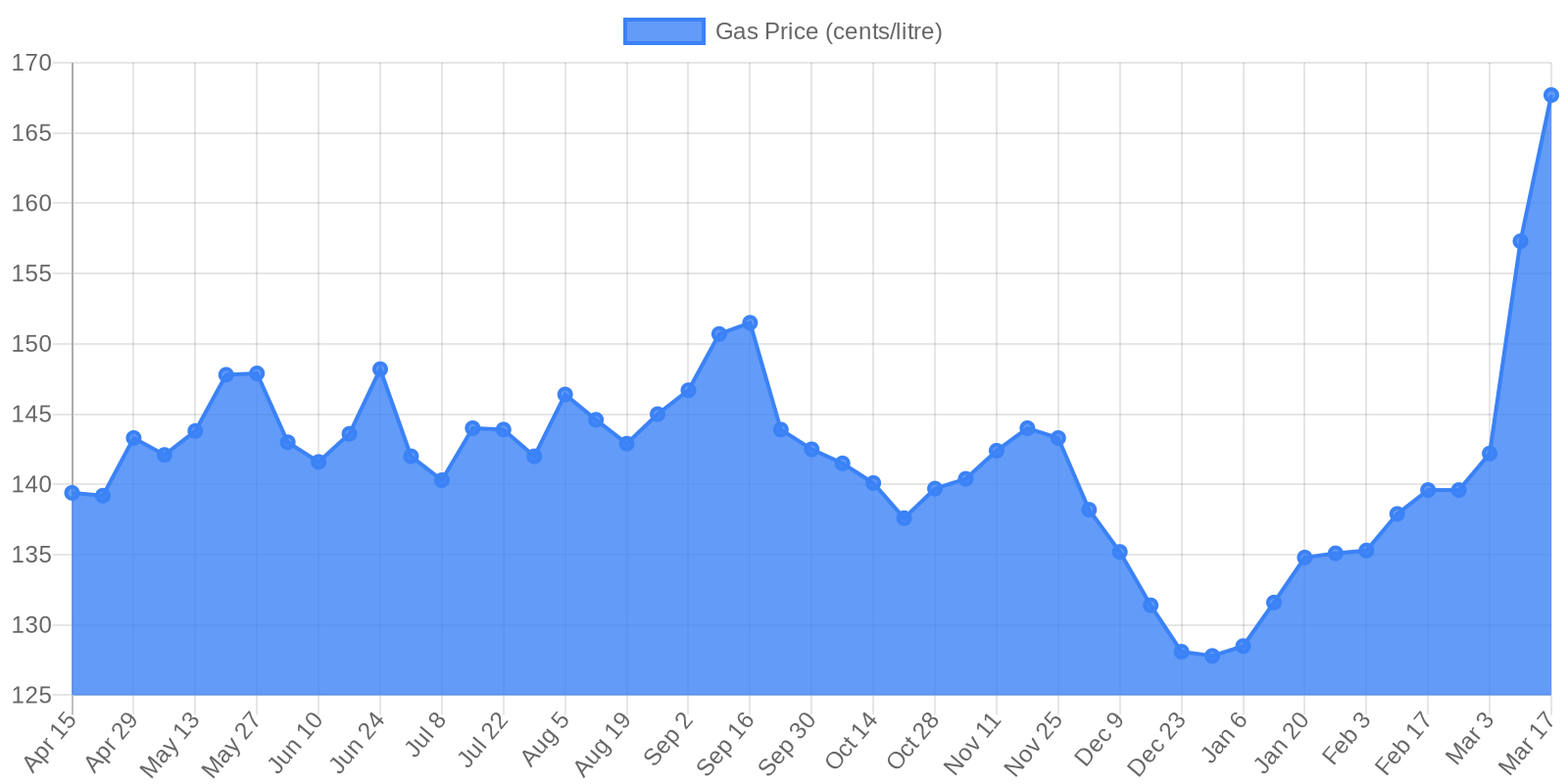

Canada's already struggling housing market just took another hit. Gas prices surged to 167.7 cents per litre in mid-March 2026, driven by the escalating conflict in the Middle East, according to data from the Financial Post. That's a 31-cent jump — roughly 23% — in just two weeks, marking the highest retail gas price since September 2024. The spike threatens to push inflation higher at exactly the wrong moment for prospective homebuyers, potentially forcing the Bank of Canada to keep mortgage rates elevated or even raise them again despite a weakening economy.

Here's why this matters more than you might think. Research from the C.D. Howe Institute published in March 2025 shows that mortgage interest costs only have a weight of around 5 percent in the Consumer Price Index but can have a big impact, especially after the Bank of Canada's tightening or loosening cycles. The problem is that mortgage interest cost inflation stood at 10.2 percent in January 2025 — despite headline inflation decreasing from its peak of 8.1 percent down to 1.9 percent. This creates a vicious cycle: higher oil prices push up overall inflation, which could keep mortgage rates high, which in turn keeps mortgage interest costs inflated, making the Bank's job of controlling inflation even harder.

So how does this feedback loop actually work? When the Bank of Canada hikes the overnight rate, mortgage interest costs increase pushing inflation higher; when the Bank lowers the overnight rate, mortgage interest costs decrease pulling inflation down. But there's a lag. For fixed-rate mortgages — which are the majority — there is a lagged effect as they gradually come up for renewal. The chart above shows gas prices had been dropping steadily from around 150 cents in September 2025 to a low of 127.8 cents by the end of December — a brief reprieve that gave inflation fighters hope. But that relief evaporated in March as geopolitical tensions pushed oil prices sharply higher. The Bank of Canada now faces a nightmare scenario: a weakening economy that normally calls for rate cuts, colliding with rising inflation from energy costs that demands rate stability or even hikes.

Canada's housing market can't catch a break. Just when lower mortgage rates in late 2025 began to show signs of stabilizing prices — with the national benchmark rising modestly in February 2026 after months of declines — this oil shock threatens to reverse that progress. The Bank has made clear it will "look through" temporary energy price spikes, but if gas stays elevated and feeds into broader inflation, mortgage rates won't be coming down anytime soon. For buyers who've been waiting on the sidelines hoping rates would drop further, the message is stark: the window may be closing faster than expected.